Are we still talking about this?

Absolutely.

Although South Africa has made advances towards moving with innovation and technology, the economy still relies heavily on cash.

The concept of cash has always been tangible. It is held, transferred, and weighed, but how many people carry around cash these days?

Synthesis Software Technologies, in partnership with Mambu and Amazon Web Services (AWS), hosted the Payments Round Table 2.0 at the Twelve Apostles Hotel in Cape Town this month. The event brought together key decision-makers from FinTech, retail, insurance, and banking sectors to discuss the future of payment modernisation in South Africa.

Moderated by Howard Feldman, the round table aimed to address the challenges and opportunities presented by payment technology and innovation in a predominantly cash-based economy. Despite the availability of digital payment methods, many low-income consumers continue to rely on cash, necessitating solutions that cater to the needs of the economy.

Modernizing Payments in South Africa

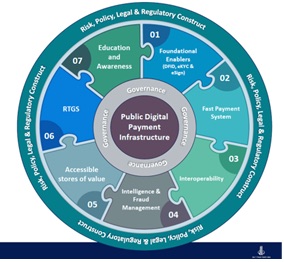

The South African Reserve Bank (SARB) has invested approximately six billion Rand in payment technologies for the public good to drive collaboration and healthy competition across key economic players. The new National Payment System (NPS) bill, closely linked to SARB’s Vision 2030, supports creation a world-class national payment utility that meets both domestic and international requirements. This bill provides a legal framework for the management, administration, operation, regulation, and supervision of payment, clearing, and settlement systems in South Africa.

The seven pillars of the Public Digital Payment Infrastructure presented by SARB Vision 2023 are highlighted below. Read more about SARB’s vision 2023.

Harsha Maloo, Head of Payments at Synthesis, highlighted the importance of financial inclusion, noting that while 80% of South Africans hold bank accounts, a significant portion remains financially excluded. Maloo presented the need for payment solutions that address the typical consumer behaviour of withdrawing cash immediately after receiving their salary.

Insights From Industry Leaders

Many households have a head who manages one account for the family. Money is deposited into an account, and technology is needed to manage the distribution of that money to other family members. Customers queue at ATMs to withdraw cash when they can withdraw cash from a retail shop and not pay bank charges for the withdrawal. A representative in the retail industry with over 700 stores across South Africa posed the questions:

“What services can retailers offer customers instead of cash in low-income and metro areas?” and “How do we look at a digital currency as a substitute for cash?”

Using a digital currency provides advantages to retailers; therefore, value propositions need to be established. Some advantages involve the saving of cash procurement and logistic fees. Retailers can be the front end of education to consumers on how to transact digitally and what is available. Many moving parts need to come together to create a platform that prioritises trust and security for consumers. To stop customers from using ATMs in the retail space, the cultural dynamics of consumer behaviour need to be considered.

Technological Innovations and Challenges

As a former executive at Solaris (a Mambu customer), Neil Capazorio, MD of ZAZU South Africa shared valuable insights from their experience working with both banks and fintech’s. They discussed the distinctions between legacy systems and third-generation technology stacks, emphasizing the transformative shift in mindset required to leverage modern solutions. Using Al and technology as enablers, ZAZU aims to address value propositions over time. Capazorio highlighted the importance of technology in simplifying the process of opening business accounts online and in real-time, thereby reducing compliance costs.

Alfred Mukudu, AWS Financial Services Go-To Market Leader, discussed AWS’s role in payment modernisation. AWS is supporting customers on platform modernisation, B2B payments, data and Al, fraud detection and prevention, real-time payments, and blockchain and digital currencies. Mukudu shared AWS’s commitment to removing technological blockers and accelerating the adoption of innovative payment solutions.

Regional and Sectoral Perspectives

Langa Mlalazi, Chief Technology Officer of Innbucks MicroBank in Zimbabwe, presented Innbucks’ innovative solution to address hyperinflation and frequent currency switches. Innbucks has created a wallet for transactions that substitutes cash, enabling rapid growth in transaction values and effectively managing high transactions per second (TPS). As part of its next phase of growth, Innbucks has partnered with leading cloud-native core platform Mambu to transform from a digital wallet solution to a fully integrated digital bank, supporting its continued expansion across Africa. Mlalazi emphasised the importance of creating a payments ecosystem that competes directly with cash. The discussion also highlighted the need for a unified African payments system to democratise different currencies, enabling seamless cross-border transfers across the continent, regardless of the local currency.

Addressing Consumer Behaviour and Trust

The round table discussion underscored several challenges and opportunities within the payment modernisation landscape.

A FinTech representative emphasised the need for banks to reduce charges and improve the usability of Payshap ID, which currently requires a banking app.

An insurance representative pointed out the anti-competitive nature of both traditional and new banks, advocating for a trusted and non-predatory ecosystem. They also noted the potential for FinTechs to offer more opportunities by reducing overhead and clearing charges and suggested that app messages could replace SMS costs.

Mlalazi stressed the importance of creating incentives for all stakeholders, while Mukudu mentioned that banks are not reluctant but face operational expenses that hinder their ability to reduce charges, suggesting partnerships between FinTechs and Banks.

Future Directions for Payments and Education

The biggest challenges identified include trust, education, value propositions for key players, profitability, culture, ecosystem awareness, traditional banks, regulation, adaptability, and transaction friction.

An insurance representative emphasised the need to start with the education system and the youth to ensure financial and digital literacy.

The broader perspective focused on solving societal problems and growing the economy in a way that benefits all stakeholders. Payments are an enabler to economic growth and should be seen as one as opposed to a revenue tool.